How much will I save if I sell my house?

A big highlight for property sellers and buyers is that, having remained unchanged since 2012, the primary residence exclusion for Capital Gains Tax has been increased from R2 million to R3 million. In addition, the annual CGT exclusion has been increased for individuals by 25% from R40,000 to R50,000, and for deceased estates by 47% from R300,000 to R440,000.

The big win is that when you sell your primary residence (the home you live in), the first R3 million capital gain is now excluded from CGT.

Have a look at the illustrative savings calculation below:

Insert table from content below

Primary residence CGT exclusion: R2m vs R3m

Old vs. new comparison

| Old exclusion: R2m | New exclusion: R3m | |

| Total capital gain | R6 000 000 | R6 000 000 |

| Less primary residence exclusion | (R2 000 000) | (R3 000 000) |

| Net capital gain | R4 000 000 | R3 000 000 |

| Less annual exclusion | (R40 000) | (R50 000) |

| Net capital gain after annual exclusion | R3 960 000 | R2 950 000 |

| Taxable capital gain (40%) | R1 584 000 | R1 180 000 |

| CGT at 45% marginal rate | R712 800 | R531 000 |

Difference in CGT payable

R712 800 − R531 000 = R181 800

Assumptions (individual, highest marginal rate 45%)

- Proceeds: R8m

- Base cost: R2m

- Capital gain: R6m

- Inclusion rate (individual): 40%

- Effective maximum CGT rate: 40% × 45% = 18%

Transfer duty threshold unchanged

Unchanged from last year, you pay no transfer duty if the property you are buying sells for at (or below) the set threshold of R1,210,000.

![]()

Source: SARS

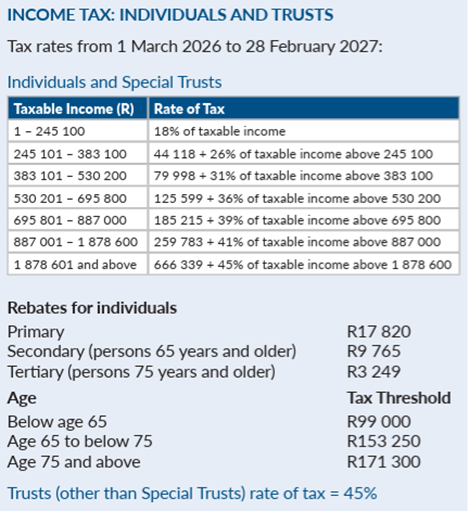

“Bracket creep” relief for taxpayers

Individual taxpayers: Your tax rates (and the associated rebates and medical tax credits) are increased in line with inflation. That’s welcome relief after last year’s unchanged tax tables which resulted in “fiscal drag” (also referred to as “bracket creep”) for anyone receiving a salary increase that pushed them into a higher tax bracket.

Trusts: Special trusts are by and large taxed as individuals, but other trusts are taxed at a flat rate of 45% – also unchanged from last year.

Source: SARS

Source: SARS

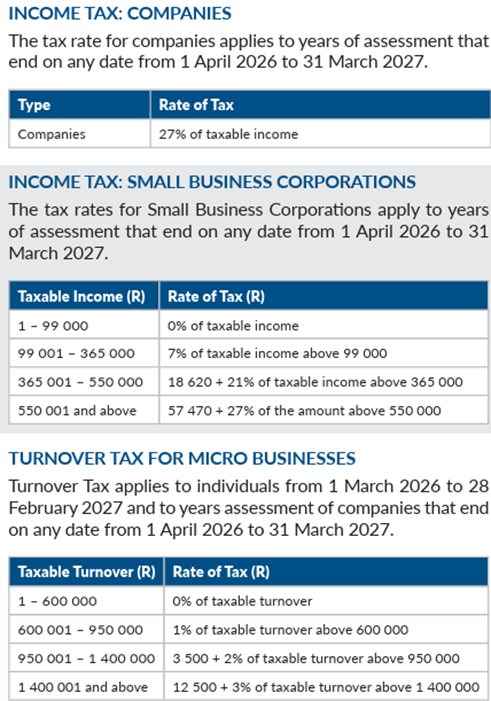

Corporate taxes: The tax rate for companies remains unchanged, with substantial relief for smaller businesses.

Source: SARS

Source: SARS

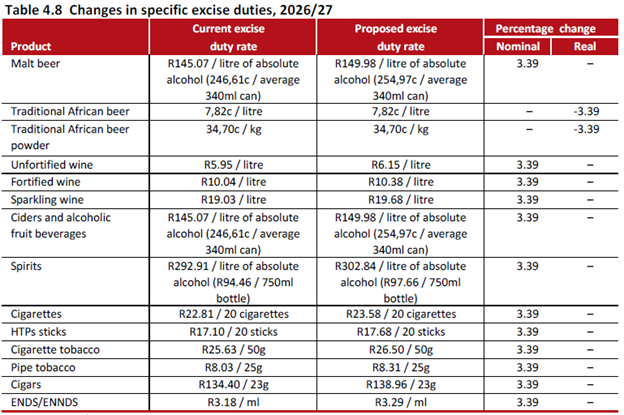

“Sin taxes” up: The details

Most sin tax increases were generally in line with or slightly below inflation. See the table below for full details.

Source: National Treasury (Table 4.8)

How much more or less will you be paying in income tax, petrol and sin taxes?

Use Fin 24’s Budget Calculator here to find out.